Describing Amazon as "the world's largest e-commerce company" is simultaneously accurate and dangerously incomplete. Accurate, because the company's roughly 37.6% share of the U.S. e-commerce market is real. Incomplete, because that framing obscures where Amazon's economic engine actually lives. In 2025, the company generated $716.9 billion in net sales — yet the vast majority of its profits came not from warehouses or shopping carts, but from data centers and ad servers. AWS alone produced $45.6 billion in operating income, while the advertising segment quietly crossed $68.6 billion in annual revenue, making Amazon the world's third-largest digital advertising platform.

Once that sinks in, a second challenge emerges: Amazon is not merely powerful — it is running one of the most aggressive infrastructure investment cycles in corporate history. Capital expenditures that stood at $77.7 billion in 2024 surged to $131.8 billion in 2025, with guidance for 2026 set at $200 billion. The unavoidable cost of that ambition is visible in the financials: free cash flow fell from $38.2 billion in 2024 to $11.2 billion in 2025. The market noticed. Amazon was the weakest performer in the Magnificent 7 for 2025, delivering roughly +5.2% versus the dramatically stronger returns of Alphabet, Meta, and Nvidia.

This is the central tension of the Amazon investment case: Is this capex a forward investment in a demand-led infrastructure buildout? Or is it a massive cycle whose returns will arrive later — and more slowly — than the market would like? This essay works through that question without flattening the complexity.

What Kind of Company Is Amazon Today? A Five-Layer Economy

Reading Amazon correctly requires treating it not as a single business but as five distinct economic layers that fund and reinforce each other.

Layer One — Retail and Marketplace. This is Amazon's visible face, and its primary function is generating volume and user base rather than high direct margins. Third-party sellers now account for more than 60% of units sold on the platform, with 1.9 million active 3P sellers making Amazon fundamentally a logistics-plus-marketplace infrastructure business. The direct margin on this layer is thin. But the cash flows it generates and the purchase data it produces are critical raw materials for the rest of the stack. Regional logistics network restructuring cut per-unit costs by approximately $0.50, and by 2025 North America operating margin reached 6.95% — a remarkable recovery from -0.90% in 2022, driven by a combination of operational efficiency gains and the rising contribution of advertising dollars.

Layer Two — AWS. This is the real profit engine. In full-year 2025, AWS generated $45.6 billion in operating income, accounting for approximately 57% of Amazon's total $80.0 billion in operating profit. The annualized run rate hit $142 billion, and Q4 2025 growth accelerated to 24% — the fastest in 13 consecutive quarters. AWS operates at roughly 35% operating margins, funding Amazon's lower-margin operations at scale. It is not merely a cloud provider; it is Amazon's financial skeleton.

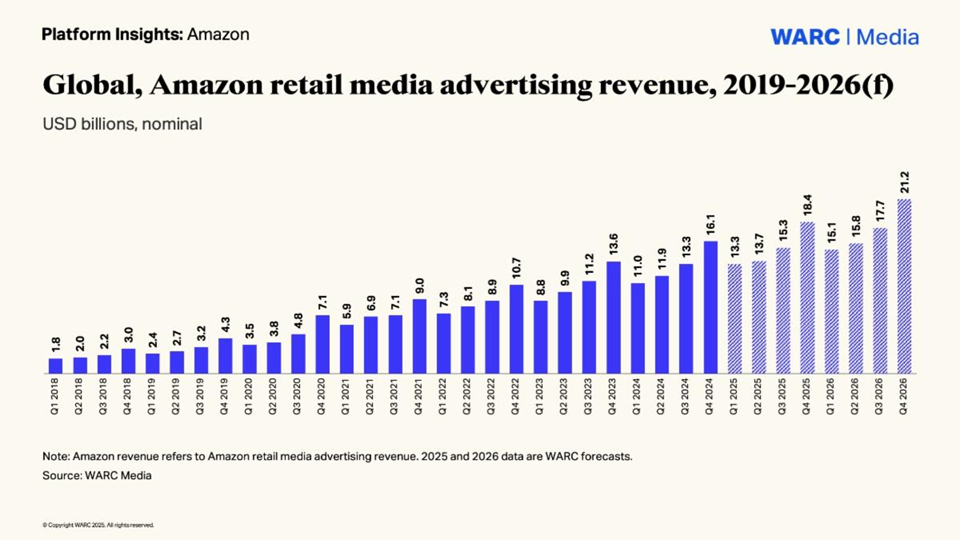

Layer Three — Advertising. Amazon's "hidden second engine" deserves that label. At $68.6 billion in annual revenue with 22% growth, this segment is approaching scale that rivals Google's YouTube alone. Q4 2025 alone produced $21.3 billion. The structural advantage advertising enjoys is distinct from anything Google or Meta can replicate: Amazon works with purchase-intent data at the moment of decision — what did the user buy, search, add to cart, then abandon? First-party shopping signals at this resolution command premium pricing, and that premium is defensible.

Layer Four — Prime and the Subscription Ecosystem. With 250 million global subscribers and roughly $49.6 billion in annual subscription revenue, Prime has evolved from a shipping loyalty program into an ecosystem binding agent. It bundles free delivery, Prime Video, Prime Music, and the Alexa ecosystem into a single monthly commitment that creates enormous switching friction. The March 2026 increase in the ad-free Prime Video tier by $2/month, and Prime Video's expansion to 315 million viewers across 16 countries, illustrate how content and advertising economics are now fused within the subscription layer.

Layer Five — AI Infrastructure and Amazon Leo. The layer with the lowest current revenue contribution but the highest forward optionality. It spans Trainium and Inferentia chips, the Bedrock platform, AgentCore, the Nova model family, Alexa+, and the Amazon Leo satellite program. None of these appear as clean standalone revenue lines today — but they are meaningfully driving the acceleration in AWS demand. The relationship between the five layers is this: retail generates the user base and data substrate; AWS produces the majority of profits; advertising converts retail data into high-margin revenue; Prime maintains ecosystem cohesion; and the AI layer provides the architectural foundation for deeper moats in 2027 and beyond.

AWS: Still the Center of Gravity

Framing AWS as merely a "cloud division" is the most costly analytical error one can make when evaluating Amazon. In 2025, AWS is not just Amazon's largest segment — it is the company's economic reason for existing in its current form. With approximately 30% global cloud infrastructure market share, AWS sits well ahead of Azure at roughly 20–22% and Google Cloud at roughly 12–13%. But market share is not the story. The story is what AWS produces: $45.6 billion in operating income at roughly 35% operating margins, funding the entirety of Amazon's lower-margin global operations.

AWS growth reaccelerated through 2025 for a clear reason: AI workloads are migrating to cloud infrastructure at meaningful scale. Enterprise companies buying large-scale compute capacity for model training and inference are doing so substantially through AWS. CEO Andy Jassy made the causal logic explicit when he stated that "capacity is monetized the moment it comes online" — a signal that this capex is responding to a demand backlog, not being built speculatively. The fact that Trainium2 capacity is entirely reserved, with no availability for new customers, is the most credible piece of evidence supporting that framing.

But AWS's significance extends beyond cloud hosting. Bedrock now catalogs dozens of models — Claude, OpenAI's GPT family, Meta Llama, Mistral, Amazon Nova, and more — making it arguably the world's broadest multi-model inference platform. This "model-agnostic distribution layer" is a strategic departure from Azure's comparatively concentrated OpenAI alignment. Enterprise customers who want optionality — the ability to switch models without re-platforming infrastructure — find that AWS offers something Azure structurally resists. That distinction matters as AI workloads become production-grade and enterprises begin to understand the long-term vendor implications of their model choices.

Advertising: Amazon's Most Underappreciated Power Source

An analyst who evaluates Amazon without treating advertising as a primary segment has made the same error as evaluating Alphabet without search revenue. The Amazon advertising business crossed $68.6 billion in annual revenue in 2025, with Q4 alone producing $21.3 billion at roughly 23% year-over-year growth. This makes Amazon the third-largest digital advertising platform globally, behind only Google and Meta — a position held by a company most investors still primarily associate with cardboard boxes.

The structural moat here is not reach. It is data specificity. Google knows what users search for. Amazon knows what they buy, what price point triggered the decision, what they added to cart and removed, which categories drive repeat purchases. This purchase-intent resolution is structurally superior to search intent for advertisers with direct commerce goals, and that superiority commands premium CPMs. The addition of Prime Video's advertising tier amplifies this — 315 million viewers are now part of Amazon's ad inventory, and that audience carries richer purchase-behavior signals than any traditional television audience.

This creates the flywheel that makes Amazon's economics coherent. Retail runs at thin margins. The data it generates flows into advertising. Advertising runs at high margins and growing scale. That margin pool subsidizes the retail cash cycle and co-funds the AWS buildout. Retail, in this framing, is not a low-quality business to be apologized for — it is the demand-generation and data-production layer that makes the high-margin businesses possible.

The Capex Cycle: Demand Signal or Delayed-Return Risk?

When Amazon disclosed its 2026 capital expenditure guidance of $200 billion in February 2026, the market's first response was a decline in the share price. The reaction was not irrational. Capital expenditures went from $77.7 billion in 2024 to $131.8 billion in 2025, and the guidance implies another step-change higher. This spending encompasses AI compute infrastructure, data center construction, networking and power capacity, dedicated compute for the U.S. government, and the Amazon Leo satellite program. The pressure this creates in the financials is visible: despite a strong $139.5 billion in operating cash flow, free cash flow in 2025 fell to just $11.2 billion because capex is growing faster than OCF.

The mechanism is straightforward. OCF is strong, but capex is growing faster — so FCF compresses. The depreciation effect compounds this: every data center and piece of equipment funded now becomes a multi-year depreciation charge against future income statements. The $200 billion being deployed in 2026 will generate amortization and depreciation loads across the next five to ten years. That full accounting burden has not yet arrived.

For a short-horizon investor, this is genuinely uncomfortable. The counter-argument — Jassy's claim that capacity monetizes immediately upon completion — is not empty reassurance. Q4 2025's 24% AWS growth and the triple-digit expansion in AI chip revenue confirm that this infrastructure is being built in response to real demand backlog, not speculative hope. The risk is specific: if that demand cadence breaks — a scenario that has precedent in technology capex cycles — the return on this investment slows materially and the depreciation burden becomes a drag without compensating revenue growth.

Segmented by time horizon: in the 0–12 month window, FCF pressure continues and the market will continue to discount this. In the 1–3 year window, the question becomes how quickly the new capacity monetizes — particularly AI inference workloads which carry strong unit economics — and whether depreciation growth stabilizes. In the 3–5 year window, the accumulated infrastructure establishes either a durable structural moat or a capital-intensive asset base that generates acceptable but unexciting returns. The 2026–2027 period is the inflection test.

A comparison with Meta is instructive. Meta also ran a large capex cycle in 2025, but Meta's AI spending flows primarily toward model development and user engagement — it does not directly sell compute capacity as a revenue-generating service. Amazon's distinguishing quality is that AWS converts capex into directly billable infrastructure. The comparison with Microsoft is more nuanced: Azure's enterprise penetration is formidable, but AWS is now hosting both Anthropic and OpenAI compute — meaning Microsoft's most powerful partner is simultaneously one of AWS's largest customers. That structural peculiarity deserves more analytical attention than it currently receives.

Anthropic and OpenAI: Why Amazon Does Not Want to Own the Model

To understand Amazon's AI positioning clearly, a conceptual distinction is essential. The model war asks: which AI model is best? The platform war asks: which infrastructure will host, distribute, and monetize all models? Amazon has made an unambiguous, consistent choice to fight the second war.

In November 2024, a $4 billion additional investment brought Amazon's total commitment to Anthropic to $8 billion. Then, in February 2026, Amazon announced a strategic partnership with OpenAI involving a $50 billion investment commitment. Treating these two moves as contradictory is a mistake. They are applications of the same logic: rather than betting on which model wins, Amazon is positioning AWS as the compute, distribution, and inference layer for every model that matters — regardless of outcome.

The Anthropic relationship is architecturally deeper. AWS is Anthropic's primary cloud and training partner, and more significantly, Anthropic participates in the design of Trainium2 chips. This co-design relationship creates mutual dependency: Trainium is optimized for Anthropic's workloads, and Anthropic's inference economics are improved by running on purpose-built silicon. The financial returns have already materialized in part: when Anthropic reached a $183 billion valuation in September 2025, Amazon's minority stake was worth approximately $60.6 billion, and Q3 2025 reported a $9.5 billion one-time accounting gain from that appreciation.

The OpenAI partnership carries different strategic weight. Under this agreement, AWS becomes the exclusive third-party cloud provider for OpenAI Frontier models. OpenAI will consume 2 gigawatts of Trainium capacity on AWS, and a Stateful Runtime Environment for OpenAI workloads will be built on Amazon Bedrock. This is a transformative commitment: it makes Trainium indispensable to the world's most prominent AI company and makes AWS the infrastructure backbone for OpenAI's production deployments. For Microsoft, the competitive implication is uncomfortable — Azure's most strategically important partner is simultaneously becoming one of AWS's largest compute customers.

The architecture of Bedrock completes the picture. Bedrock today hosts Claude, GPT models, Meta Llama, Mistral, Amazon Nova, and more in a unified interface. For enterprise customers, this means a single infrastructure layer enables them to run any model of their choosing without re-platforming. That "model-agnostic distribution" function is what Amazon is actually building — not a model, but the layer beneath all models.

Trainium, Nova, AgentCore, Alexa+: How Real Is the AI Stack?

Evaluating Amazon's AI stack honestly means resisting two symmetric temptations: overstating its competitive differentiation and dismissing it as cosmetic packaging for AWS. The reality is more precise — each component has a specific functional role that materially strengthens AWS economics, without any single component qualifying as a standalone market leader.

Trainium and Inferentia represent Amazon's strategy to reduce NVIDIA dependency. Trainium2 capacity is fully reserved; Trainium3 was announced at AWS re:Invent 2025 with claims of roughly 40% better price-performance versus H100. The combined Trainium and Graviton revenue run rate is estimated to exceed $10 billion annually. The honest framing here is that Trainium is not a NVIDIA replacement — it is a cost optimization tool for specific training and inference workloads. NVIDIA's software ecosystem, developer tooling, and general-purpose capability remain substantially ahead. But at $200 billion in annual capex, even marginal unit economics improvements represent enormous absolute dollar savings.

Amazon Nova — the native model family launched in December 2025 with Nova 2 Lite and Pro — is not positioned as a frontier model competitor to Claude or GPT-4. Its function within Amazon's strategy is more specific: to provide a cost-effective, fast, capable-enough native model option on Bedrock that reduces the fraction of workloads that require expensive frontier models. Nova is a Bedrock margin management tool rather than a market leadership play.

AgentCore — launched at AWS re:Invent 2025 — is an enterprise infrastructure layer for agentic AI: systems that autonomously execute multi-step tasks. Early customer metrics cited include 24,000 hours of work automated and 63% autonomous resolution rates for certain process categories. Agentic AI is the fastest-growing enterprise AI category in 2025–2026, and AWS's platform positioning here creates meaningful customer lock-in. If enterprises build production agent workflows on Bedrock AgentCore, the switching costs are substantial.

Alexa+ — launched in February 2025 at $19.99/month, or free for Prime members — attempts to place an agentic AI assistant on top of 600+ million Alexa device endpoints. The strategic logic is compelling: virtually no other company has that hardware footprint as a starting point. The monetization uncertainty, however, is real. By offering it free to Prime subscribers, Amazon is using Alexa+ primarily to increase Prime stickiness rather than building an independent revenue stream. In a market where Apple Intelligence, Google Gemini, and ChatGPT are all competing for the same user behavior, Alexa+'s differentiation remains to be demonstrated.

The honest summary: Amazon's AI stack is functional, purposeful, and increasingly integrated — but it operates primarily as a set of reinforcing components within the AWS platform rather than as a collection of independent, category-defining businesses. That distinction matters for how quickly these investments appear in reported financials.

Amazon Leo: An Expensive Option — But Not Without Strategy

The analytical discipline required for Amazon Leo is to avoid two common failure modes: dismissing it as a financially irrelevant vanity project chasing SpaceX, or inflating it into an automatic long-term value catalyst. The truth is more specific and more conditional.

The current state is clear. Twenty-seven operational satellites were launched in April 2025, and approximately 200+ are in orbit as of late 2025. The target constellation is 3,236 satellites. Against this, Starlink has launched more than 8,000 satellites, operates commercial service in over 100 countries, and has both individual and enterprise customer bases at scale. Amazon Leo is not competitive with Starlink today in any consumer or commercial broadband sense. FCC interim deadline pressure — requiring approximately half the planned constellation in orbit by July 2026 — creates an urgent launch cadence that introduces execution risk. In the near term, Amazon Leo carries a meaningful balance sheet cost with no revenue contribution, and it was flagged in Q4 2025 guidance as a drag on operating income.

That said, the strategic logic is not fabricated. Amazon has three credible reasons to continue the program. First, AWS edge connectivity: a global broadband infrastructure layer would remove a real constraint on AWS's ability to serve enterprise customers in connectivity-limited geographies. Second, government and defense: classified and sovereign networks for U.S. and allied defense and intelligence agencies represent a segment where non-terrestrial connectivity has genuine strategic value — and where Amazon already has deep classified cloud relationships through AWS. Third, vertical-specific enterprise applications — maritime, aviation, energy, and remote industrial operations — where Starlink's consumer-adjacent model may create pricing and service-level differentiation opportunities for a more enterprise-focused offering.

The distinguishing factor Leo could eventually deploy is AWS integration depth. Data traffic flowing through Leo terminals could connect directly to AWS compute and storage without terrestrial routing. For enterprise and government customers, that integration advantage could matter more than raw speed or price. This is a 2028–2030 thesis, not a 2026 thesis. For today's investor, Leo is an option that costs money and delivers no return in the near term. Whether that option proves valuable depends on execution quality, competitive dynamics with Starlink, and the pace of AWS enterprise broadband demand development — none of which is knowable with confidence today.

Equity Impact Map: Who Benefits, Who Faces Pressure?

Amazon's $200 billion capex cycle does not affect only AMZN. The first and second-order effects across the technology ecosystem are worth mapping carefully.

NVIDIA (NVDA) remains Amazon's most important chip partner in absolute terms. Amazon explicitly describes its NVIDIA relationship as "extremely important" and continues placing large orders for H100, H200, and Blackwell hardware. Trainium's ability to absorb some incremental workloads creates modest long-term headwinds for NVIDIA's AWS share, but in the near term, Amazon's infrastructure buildout is a net positive for NVIDIA demand. The risk to this thesis is if Trainium3 benchmark claims prove out at scale and OpenAI's decision to run on Trainium capacity signals a broader shift in hyperscaler AI chip preferences.

AMD (AMD) benefits more modestly. AWS maintains multi-vendor chip diversity including NVIDIA, AMD, and Intel, and AMD's MI300X GPU is present in Bedrock's compute catalog. But with NVIDIA dominant and Trainium growing, AMD's incremental share of Amazon's capex expansion is limited. Slight positive, not a primary catalyst.

Broadcom (AVGO) and Arista Networks (ANET) are the cleanest infrastructure beneficiaries in Amazon's buildout. Broadcom captures custom networking ASIC and semiconductor demand; Arista is the leading name in high-scale AI data center networking. Both companies benefit directly from the pace and scale of Amazon's $200 billion annual capex cycle. The primary risk for both is a general hyperscaler capex slowdown — if demand for AI infrastructure decelerates, both feel it simultaneously across multiple customers.

Microsoft (MSFT) occupies the most complex competitive position in relation to Amazon. Azure continues growing at approximately 33%, and the Copilot ecosystem deepens enterprise penetration. But the OpenAI partnership dynamics create a structural paradox: Microsoft's most strategically valuable partner — OpenAI — is simultaneously consuming 2 gigawatts of Trainium capacity on AWS and has designated AWS as its exclusive third-party cloud provider for Frontier models. This does not directly cannibalize Azure's existing workloads, but it does create ambiguity around the narrative that Azure is OpenAI's natural home. A mixed picture for the medium term.

Alphabet / Google (GOOGL) is growing Google Cloud at approximately 32%, making it the fastest-growing major cloud platform. Gemini's integration across Google Workspace and the TPU ecosystem represent genuine competitive pressure on AWS. Notably, Google has also invested $3 billion+ in Anthropic — meaning Amazon's flagship AI investment does not provide exclusive competitive protection. Alphabet faces the most direct structural competition from AWS's AI workload growth among the major cloud peers, but its own strong momentum largely offsets that pressure in the current period.

Oracle (ORCL) has built a meaningful niche in enterprise and government cloud. However, AWS's $50 billion U.S. government investment plan and the opening of its second classified cloud region apply direct pressure on Oracle's most defensible market segment. Oracle's participation in the OpenAI Stargate initiative partially offsets this, but the net effect on Oracle's government and enterprise cloud positioning is negative at the margin.

Salesforce (CRM) is a conditional beneficiary. A new AWS partnership agreement was signed in Q4 2025, and Salesforce's Agentforce platform runs on Bedrock. As long as Amazon's agentic AI infrastructure enables Salesforce's workflows rather than competing with them, this is a positive relationship. The risk scenario is if Amazon's AgentCore begins addressing enterprise workflow automation use cases that Salesforce currently owns — a competitive dynamic that is real but not yet acute.

Walmart (WMT) faces ongoing pressure from Amazon's retail execution. The roughly $0.50 per-unit logistics cost reduction, the scale of same-day delivery operations, and Amazon's 3P marketplace depth continue to compound competitive distance. Walmart's own digital commerce growth is meaningful, but the structural pressure from Amazon's logistics efficiency machine is persistent.

Anthropic is the company most directly aligned with Amazon's AI strategy. As AWS's primary training and inference partner, the beneficiary of Trainium co-design, and a company whose equity has already returned $60.6 billion in paper value to Amazon, Anthropic sits in a position of mutual dependency with Amazon that is both financially and strategically reinforcing. The risk scenario is OpenAI's competitive ascent reducing Anthropic's market position — but even in that scenario, Amazon's platform neutrality via OpenAI's AWS compute relationship provides a hedge.

SpaceX / Starlink faces a credible but distant competitive threat from Amazon Leo. The enterprise satellite broadband and government connectivity markets are the arenas where Leo eventually competes. Near-term, Starlink's 8,000+ satellite lead, operational maturity, and customer relationships make the competitive impact minimal. In a 2028–2030 scenario where Leo achieves meaningful scale and AWS integration delivers differentiated enterprise value, the government and enterprise segments could see genuine competition. SpaceX is private, but this dynamic is relevant for any investor tracking classified and enterprise satellite connectivity contracts.

The Bullish and Bearish Cases, Honestly Weighed

A serious analysis cannot resolve into a single directional call. Both the bull case and the bear case for Amazon carry real substance.

The strongest bullish arguments. AWS growth is not merely sustaining momentum — it is re-accelerating. The Q4 2025 24% growth rate, occurring against what was already a large base, reflects the early-stage migration of AI workloads to cloud infrastructure. As enterprise companies move AI models from experimentation to production, inference demand grows nonlinearly — and AWS is positioned to capture a large share of that demand. The Trainium strategy creates structural cost advantages over time: at $200 billion in annual capex, even modest improvements in chip unit economics translate to billions in margin protection. The dual positioning with Anthropic and OpenAI — holding meaningful equity in the former while providing exclusive compute infrastructure for the latter — creates a platform advantage that is difficult to replicate. The advertising business is high-margin, growing fast, and structurally defensible. And retail's margin recovery from deeply negative territory to nearly 7% demonstrates operational discipline that the market likely undervalues.

The strongest bearish arguments. Free cash flow fell to $11.2 billion in 2025 and the $200 billion 2026 capex guidance will suppress it further. The depreciation effect from this spending cycle has not fully arrived. AI revenues remain largely indirect — Trainium and Bedrock are described as "multi-billion dollar" businesses, but they are not broken out as separate income statement lines, making them difficult for investors to model with precision. The Anthropic and OpenAI partnerships generate indirect platform benefits whose net monetization is genuinely uncertain: if either model company begins building proprietary compute infrastructure at scale, AWS's compute dependency relationship weakens. Amazon Leo is a balance sheet burden with no near-term return trajectory and execution risk around FCC deadline compliance. And the market has already rendered a judgment: Amazon was the weakest Magnificent 7 performer in 2025 despite strong operational results. That discount reflects the capex-return timing uncertainty, and it will persist until FCF normalization becomes visible — which is unlikely before late 2027.

The dispassionate synthesis: Amazon is running a structurally sound business at exceptional scale. But a structurally sound business does not guarantee satisfying equity returns on any particular time horizon. The capex-to-free-cash-flow compression creates a patience tax for shareholders. Until the market develops confidence in the return timeline, Amazon's premium to the market will remain contested.

Final Synthesis: What Is the Market Pricing, and Where Is the Asymmetry?

Have recent developments changed the investment thesis materially? Partially yes, meaningfully not yet. The reacceleration of AWS growth to 24% and the accumulation of $45.6 billion in operating income strengthen the foundational thesis. The $60.6 billion appreciation in Amazon's Anthropic stake and the OpenAI partnership — designating AWS as exclusive third-party cloud for Frontier models — validate the "whoever wins the model war, I host the compute" logic in operational reality rather than concept. These are genuine thesis-strengthening developments.

What they have not resolved is the capex return timeline. The $200 billion 2026 guidance makes FCF normalization a 2027 event at earliest. Until that normalization becomes visible in quarterly results, the market will continue applying a discount to Amazon relative to peers whose AI investment is more directly monetized in reported financials.

Where is the asymmetry? The advertising segment is a strong candidate for underappreciation. At $68.6 billion annually with 22%+ growth and high margins, the Amazon advertising business on a standalone basis would be among the most valuable digital advertising properties in the world. But because it sits inside a conglomerate structure alongside low-margin retail, its margin quality and growth profile are not fully apparent in consolidated financials. Investors who recognize the segment economics separately may be looking at a business that trades at an implicit discount to what it would command independently.

The deeper asymmetry is in timing. The Trainium plus Bedrock plus OpenAI compute guarantee combination has a specific financial implication: AWS's incremental revenue per dollar of capex should improve as dedicated AI compute capacity fills at contracted rates. If AWS sustains 20–25% growth through 2026 and FCF normalization begins in 2027, the current share price may represent the market's most skeptical view of a platform that, structurally, is becoming harder to compete with — not easier.

Amazon today is a platform company of extraordinary breadth and depth. It simultaneously anchors the retail economy, hosts the AI computation of the world's two most powerful model builders, generates nearly $70 billion per year from high-margin advertising, and is building a satellite constellation that could eventually connect its cloud to the physical world without terrestrial intermediaries. The market is not fully rewarding this because the path from massive investment to normalized free cash flow is not yet clear. But the path has a logic to it — and for investors whose time horizon extends past the FCF compression trough, the question may not be whether Amazon wins, but when the market decides to believe it already has.